- Unfortunate regression in fatalities primarily due to the Burnstone conveyor contractor incident

- Revenue 18% lower than for 2022, primarily due to lower PGM and nickel prices

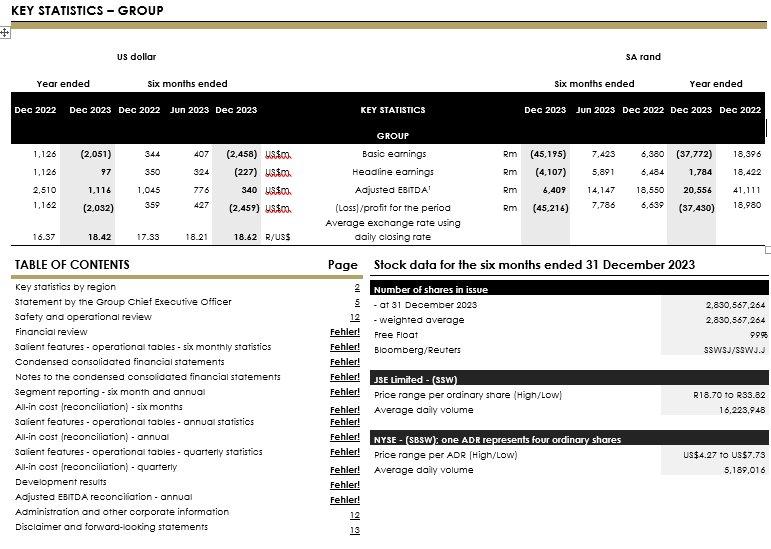

- Loss for the period of R4bn (US$2.0bn) includes non-cash impairments of R47.5bn (US$2.6bn)

- Zero final dividend together with interim dividend of 53 SA cents per share (11.19 US cents* per ADR) equivalent to an annual yield of 1%

- Proactive repositioning to rebase high-cost operations expected to deliver R6.6 bn in cost savings and capital preservation

- Strong balance sheet at year-end with net debt: adjusted EBITDA at 58x

- 1bn (US$412 million) adjusted EBITDA turnaround in SA gold

- SA PGM operations continue to move operations down the industry cost curve with 4% unit cost increases

- Construction of the Keliber lithium refinery commenced in Q1 2023 and concentrator earth works started in Q4 2023

* Based on the closing exchange rate of R18.94/US$ at 22 August 2023 from EquityRT and closing share price of R24.90 at 31 December 2023

STATEMENT BY NEAL FRONEMAN, CHIEF EXECUTIVE OFFICER OF SIBANYE-STILLWATER

While the operating environment remains challenging, with macro-economic and geo-political uncertainty persisting, our medium to long term view on the fundamental outlook for the metals we produce with the exception of nickel, remains largely unchanged.

We are confident that the PGM price weakness during 2023 does not signal a structural change in PGM fundamentals like that of the nickel market, but is more temporary in nature and we are beginning to see increasing signs which support a better demand outlook. We believe that the precipitous decline in PGM prices during H1 2023, was due to a confluence of negative factors and exacerbated by unexpected destocking of inventory which caught the market by surprise, causing increased uncertainty and market anxiety. This bearish sentiment was reflected in a significant build-up of speculative short positions in palladium, which also contributed to the price pressure.

We continue to see emerging signals that in fact support our long held, robust view on the PGM demand including:

- Absolute light duty vehicle (LDV) production is forecast to grow over the rest of this decade

- The recent moderation in battery electric vehicle (BEV) growth rates and accompanying increase in hybrid power-train adoption supports our view that the predicted demise of internal combustion engine (ICE) vehicles was premature and that delivery on BEV penetration forecasts would be challenging

- Primary supply is likely to continue declining in an inflationary environment with low PGM prices

- Recycling supply remains subdued and well below forecasts

At the same time, we remain constructive on the outlook for lithium as well, despite current oversupply and the collapse in lithium prices. We see increasing evidence that permitting and financing new mine supply is becoming more challenging and costly. As such we remain confident that we have timed our lithium strategy well and will be suitably positioned to deliver into a growing deficit market in the latter part of this decade.

Despite this relatively sanguine view on future metal prices, we are not ignorant of the risks posed by a potential extended downturn, and have already taken proactive and decisive actions, which tangibly address financial losses and better position the business for sustainability.

Our repositioning for a changing and less supportive environment began in 2021, aligned with our revised strategy, which was informed by the grey elephants (highly probable, high impact and yet ignored threats) we identified at the time.

The initial repositioning commenced in mid-2022 in anticipation of a deteriorating operating environment and palladium price outlook, with the US PGM operations repositioned for the high inflation environment, by suspending capital expenditure on further growth and a refocus on improving operational flexibility and efficiency and reducing costs.

The significant further decline in palladium and rhodium prices during 2023, was larger than we had anticipated, prompting a Group wide review of all operations and a focus on bottom of the cycle austerity and value preservation.

The identification and decisive implementation of cost saving and capital preservation opportunities during 2023 and 2024 to date, is expected to yield approximately R6.6 billion (US$375 million) in cost and capital savings (aiming at resetting the cost base) and capital reduction and/or deferrals, which will benefit near and medium term cash flow. These initiatives since mid-2022 include.

We recognize however that if low commodity prices persist, earnings are going to remain under pressure and, with ongoing inflationary cost pressure, there may be further restructuring required. We have a strong balance sheet as a buffer, but will clearly continue to manage our financial position in terms of our earnings and cash flow.

This may require further repositioning to address losses at the US PGM operations and the Sandouville refinery. The recent Court ruling on aspects of the Keliber lithium project is likely to result in delays to the commencement of the Rapasaari mine. While further assessment of the implications for the Keliber Lithium project are still being done, rescheduling of some capital investment may be an option. We are also considering alternative capital and financing opportunities including revenue protection and monetisation and in 2023 implemented a hedge at our SA gold operations of over 60% of 2024 production, with a floor of R1.1m/kg and a ceiling of R1.4m/kg, protecting revenue downside without stifling upside.

Safety

A regression in the number of fatal incidents in 2023 compared to 2022 (which represented a record year for most safety measures) was deeply regretful and of concern for management and the board was the increase in number of fatalities to 11 from five in 2022. Despite this disappointing regression in fatal incidents, our continued focus on eliminating fatalities through the ongoing implementation of the fatal elimination plan Group wide, resulted in many improvements in underlying safety trends during the year.

The safety performance of the Group is covered in more detail on page 12 of this report, but on behalf of management and the Board of Sibanye Stillwater, we wish to express our deep regret and extend our sincere condolences to the families and friends of our late colleagues.

We are committed to continuous improvement in health and safety at our operations. This is a deliberate journey and whilst we have made significant progress, we continue to embed the strategy based on lessons learned and industry best practice to improve our high energy risk mitigation approach thereby eliminating fatalities from our operations. Pleasingly during 2023, we achieved a best ever performance in serious injuries and a significant reduction in incidents and injuries that had a potential for loss of life. Our SA PGM operations achieved over 11 consecutive months fatal free while our gold operations have currently been fatal free for seven months. Our absolute priority remains on eliminating fatal incidents from our operations.

Financial overview

The substantial declines in the prices of most commodities (with the notable exception of gold) and persistent cost inflation, translated into materially lower earnings and cash flows placing the entire global mining industry under severe financial pressure.

The Group’s financial results for the year ended 31 December 2023 (2023) were similarly impacted by the sudden and sharp decline in PGM and nickel prices. The 33% year-on-year decline in the average PGM basket prices in particular, resulted in a dramatic fall in the profitability of the US and SA PGM operations, which in recent years have contributed the bulk of Group earnings and cash flow.

The contrast in profitability of these operations between H1 2023 and H2 2023 is particularly stark, with the average 2E PGM basket price declining by 19% period-on-period to US$1,124/2Eoz (R20,928/2Eoz), resulting in the US PGM operations reporting an adjusted EBITDA loss of US$18 million (R266 million) from adjusted EBITDA of US$53 million (R976 million) for the previous 6 months. While the SA PGM operations remain profitable, a 42% decline in the average 4E PGM basket price resulted in adjusted EBITDA more than halving period-on-period to R5.8 billion (US$309 million) for H2 2023.

Consequently, Group adjusted EBITDA for 2023 fell to R20.6 billion (US$1.1 billion), 50% lower than adjusted EBITDA of R41.1 billion (US$2.5 billion) for 2022, which was in itself a 40% decline from record levels of R68.6 billion (US$4.6 billion) for 2021 (which marked the peak of the commodity price cycle).

The significant decline in metal prices and uncertain outlook, along with specific operational performance factors, also resulted in the Group having to recognise impairments of R47.5 billion (US$2.6 billion) against various assets (detailed in the condensed consolidated financial statements), which was a primary driver of the Group reporting a loss for 2023 of R37.4 billion (US$2.0 billion) compared with a R19.0 billion (US$1.2 billion) profit for 2022.

Pleasingly however, other than the US PGM recycling business, which continued to be impacted by external factors, all of the Group’s operations achieved production guidance for 2023 with our SA gold and SA PGM operations and Australian retreatment operation, Century zinc, all profitable before the end of Q4 2023.

Consistent and disciplined adherence to the Group capital allocation framework, has also maintained a solid financial position at year-end, with our balance sheet leverage still well below our stated mid-cycle comfort ratio of 1x net debt:adjusted EBITDA, with cash on hand of R25.5bn (US$1.4bn) and undrawn debt facilities of R24bn (US$1.29bn) providing ample liquidity headroom and financial flexibility.

ESG and Sustainability – commitment and success

Sustainability/ESG is a strategic imperative for the Group and Sibanye-Stillwater continues to drive ESG improvement throughout the Group. To advance this commitment, Melanie Naidoo-Vermaak was appointed as Chief Sustainability Officer, effective 1 January 2024. Melanie has over 20 years’ experience in sustainable development in both the private mining and public sectors in South Africa and globally. In addition to driving our efficient delivery of our strategic ESG priorities, Melanie will also will further diversify and strengthen our senior leadership team. (https://www.sibanyestillwater.com/about-us/leadership/melanie-naidoo-vermaak/).

In 2023 notable achievements have been made in the following areas:

We have made considerable progress with our SA renewable projects which will further reduce our carbon footprint, energy security risk and improve operating costs, thereby enhancing the sustainability of our SA operations. There are currently 632MW of renewable projects planned in SA for commercial operation by end-2026 with 267MW already contracted through Power Purchase Agreements (PPAs) and in construction. The 89MW Castle wind farm, the 103MW Witberg wind farm and the 75 MW (of 150 MW) SOLA Group solar project.

These projects are expected to reach commercial operation in 2025 and will provide approximately 15% of our SA electricity requirements and will enable scope 2 emissions reduction of approximately 921,000t CO2 per year from a base of 6.7Mt combined Scope 1&2 in 2022.

A further five renewable energy projects with a total capacity of 364MW are well advanced and planned for financial close in 2024. The total project portfolio of 632 MW will supplement approximately 30% of our utility supply, with renewable electricity from 2027 provided at a 20-30% discount to Eskom tariffs, escalating at CPI. The total capital investment of these projects is c.R12-14bn, funded through third-party PPAs. In addition all projects meet or exceed the South African Mining Charter requirements and will contribute towards socioeconomic development of our local communities.

In January 2023: Sibanye-Stillwater was included in the Bloomberg Gender-Equality Index (GEI) for 2023. The Group is one of 484 companies globally (and one of only eight South African companies), across 45 countries and regions representing 11 sectors, which qualified to be included in the index. Sibanye-Stillwater was included in this year’s index for scoring above a global threshold established by Bloomberg for gender equality across five pillars: leadership & talent pipeline, equal pay & gender pay parity, inclusive culture, anti-sexual harassment policies, and external brand.

The Sibanye Foundation NPC performs public benefit activities for the benefit of the beneficiaries, with a particular emphasis on conservation, environment, healthcare, education, skills development, welfare, humanitarian, access to digital media, sports, infrastructure and cultural initiatives. In 2023, R211million (US$11million) funding was provided through allocation equivalent to 1.5% of declared dividends for societal upliftment, with R42 million (US$2 million) allocated mostly to SA where we partnered with organisations such as Gift of the Givers and Breadline Africa to providing infrastructure to disadvantaged schools in SA. One project was supported in Europe (€30,000) at a community centre. It is intended that the remaining funds will be disbursed on an annual basis to ensure continuity of the social programmes supported, to cover periods of reduced dividends.

In May 2023 Sibanye-Stillwater’s Corporate and South African operations achieved ISO 27001 certification. ISO 27001 is a globally recognised standard that sets out the requirements for an Information Security Management System (ISMS). It provides a systematic and risk-based approach to managing and protecting sensitive information, including financial data, intellectual property, customer information, and other critical assets. ISO 27001 certification is essential for protecting our employee and client information, reputation and other sensitive information. The ISO standard includes a process-based approach to initiating, implementing, operating, and maintaining our ISMS.

In July 2023, Sibanye-Stillwater and the University of the Witwatersrand, Johannesburg (Wits) launched the newly refurbished and rebranded Wits Sibanye-Stillwater Innovation bridge (the Innovation bridge), a Wits Centenary Project funded by Sibanye-Stillwater. The launch of the Innovation bridge on 12 July 2023 was accompanied by an additional commitment of R51 million from Sibanye-Stillwater to Wits for study bursaries, learnerships within the Group’s mining operations, graduate internship programmes and staff development within the Wits Faculty of Engineering and the Built Environment (FEBE). Since 2014, Sibanye-Stillwater has enabled over 500 students to study at Wits by providing bursaries and allowances amounting to R19.4 million. In addition, The Group has contributed R68.5 million in funding for the DigiMine, with a further R5.5 million committed for 2023 and has donated R50 million worth of technical equipment to the FEBE.

Good progress has been made at Marikana on the journey of the Marikana Renewal Process. As part of the Marikana renewal, we were able to collaborate with stakeholders as follows:

- Meaningful progress on the issues raised by families to the company (education, housing, livelihoods, health of the elderly and Koppie Memorial)

- Stakeholder Pitso (a gathering or conference) to look at sustainable relationship building and rebasing trust

- Agreed on a socio-economic compact delivering youth development and job creating programmes in partnership with communities, suppliers and development agencies

At the 4th annual Marikana Memorial Lecture on 14 August 2023, Gift of the Givers Founder Dr Imtiaz Sooliman, appealed to government, business, mining companies and the country’s people to work together to rebuild the country and for people to turn away from the widespread negativity which is inhibiting attainment of this goal. He said much of the negativity is due to the fact that people have not recovered from the trauma of the COVID-19 pandemic and that there are other historical factors that also need to be overcome.

Also in August 2023, Sibanye-Stillwater achieved joint first place in both the metals and mining sector category and joint first place “overall” in the 2023 sustainability data transparency index (SDTI) research report compiled by Integrated reporting & assurance services (IRAS). The SDTI is compiled annually by IRAS and the current results are based on the Sibanye-Stillwater Group’s 2022 disclosures published in April 2023 (its Integrated report and the supplements of its suite of reports). The Group scored 90.75% for the 2023 STDI – significantly higher than the mining and metals sector’s average rating of 64.5%, resulting in the top rating, further improving last year’s ranking of being third overall and the top-rated in the mining sector.

In December 2023 Sibanye-Stillwater through the Sibanye Rustenburg Mine Community Development Trust (SRMCDT) announced an R84 million investment for development programmes that will empower communities adjacent to Sibanye-Stillwater’s Rustenburg operation in the North West Province. The SRMCDT was established in 2016 by Sibanye Rustenburg Platinum Mines (SRPM) – now Sibanye-Stillwater’s Rustenburg operation – to contribute towards socio-economic development programmes to create sustainable and empowered communities within the Rustenburg Local Municipalities (exclusively SRPM communities) and create a future that will sustain them beyond mining. The Trust, which is part of the broad-based, black economic empowerment consortium owning 26% of the Rustenburg operation, has to date received an accumulative R301.8 million in dividends from the Rustenburg operation to unlock the value that can be created by community upliftment initiatives as outlined in the SRMCDT deed. The Trust supports programmes in education and training, sustainable health and social development, rehabilitation of the natural environment, training for entrepreneurs and upliftment programmes for the vulnerable in the communities, in particular women, youth, and people living with disabilities.

More recently, on 14 February 2024, Sibanye-Stillwater was awarded an ‘A-’ rating for both its water security and its climate change disclosures by CDP, a non-profit organisation which runs the global environmental disclosure system. The Group’s water CDP rating improved from B to A- and is notably higher than the average global submissions which hold a C-rating, the average C-rating for the African region, and the average B- rating for the Metallic mineral mining sector. Furthermore, Sibanye-Stillwater’s Climate change CDP rating of A- exceeded the average C-rating of the global submissions, the average B-rating for the African region, and the Metallic mineral mining sector’s average C-rating .

MARKET OVERVIEW

Green metals

PGM market – 2023

The platinum price was volatile in 2023, decreasing by 8% by year-end. The price began the year at US$1,074/oz but retreated close to US$900/oz in February. Concerns over the impact of South African power disruptions on primary supply saw the price rally to over US$1,100/oz in April. However, the producers were able to mitigate the impact with limited effect on mined volumes. The price retreated over the second half of the year, as load-shedding eased, with prices falling to a low of US$845/oz in November, before rallying to end the year at $992/oz.

The palladium price continued its retreat from the record level seen in 2022 following the Russian invasion of Ukraine, falling 39% from $1,793/oz to $1,104/oz as at 31 December 2023. Some automakers that had built up additional palladium inventory as a precaution in case of supply disruptions reduced excess stock levels during the year. In addition, Nornickel postponed its smelter maintenance resulting in higher palladium output than anticipated.

The rhodium price continued to decline, falling 64% from $12,250/oz to $4,425/oz. Similar to palladium, stock sales also influenced the rhodium price. Chinese glass manufacturers that had thrifted rhodium from their processing, owing to the high price, sold the metal into the domestic market, resulting in significantly reduced imports into China.

Light vehicle production exceeded initial expectations of modest growth and climbed 10% to almost 91 million units with global BEV production rising by 39% to over 11 million units (~12%), as supply chain disruptions were overcome and consumer demand remained robust. Automotive demand for platinum increased by 20% year-on-year to 3.3Moz, partly as a result of the increased production and partly owing to the more widespread use of tri-metal gasoline autocatalysts. Heavy-duty vehicle production increased last year, mostly as a result of higher output in China as the economy normalised following the removal of Covid-19 restrictions.

Cautious consumers in China with a preference for gold over platinum jewellery contributed a 6% decline year-on-year as net global platinum jewellery demand remained flat at 1Moz. Despite strong growth for platinum in the glass and chemical sector, overall demand for industrial uses remained flat.

Gross palladium automotive demand remained largely flat at 8.4Moz. Despite the rise in light vehicle production, palladium demand was impacted by substitution with platinum in gasoline autocatalysts.

Secondary supply of PGMs fell by approximately 14% last year as the availability of spent autocatalysts was constrained by lower scrappage rates of second-hand vehicles and some collectors held onto catalysts waiting for a recovery in prices.

In 2023, the platinum and rhodium markets shifted into deficit (~320koz and ~55koz respectively) from a surplus in the previous year, while the palladium market deficit expanded (~1Moz).

PGM market outlook – 2024

Global PGM production is expected to be slightly lower than last year. Some high-cost production has been closed in South Africa and Eskom remains a risk to refined PGM output. Last year, load curtailment was a contributing factor to the build-up of partially processed material and further high-level load shedding would make it more difficult to process this stock. Russian production is expected to be lower this year as Nornickel undertakes smelter maintenance. The autocatalyst recycling environment remains challenging. Despite a strong year for new light vehicle sales in 2023, there have been fewer end-of-life vehicles than typical as second-hand vehicles have been kept on the road for longer.

Light vehicle production is forecast to increase modestly to 91.6 million units after strong production growth in 2023 (90.8 million) as supply chain problems were overcome amid robust consumer demand. However, global BEV market share is predicted to increase to 15% from 12% resulting in slightly lower automotive demand for PGMs. The next round of European tailpipe emissions standards for light vehicles (Euro 7) has been delayed with permissible emission levels weakened, which may help to sustain PGM demand in autocatalysts. While this does not offer the higher PGM loadings normally seen at each new step in emissions standards, it also does not add significant cost to internal combustion engine vehicles, thus keeping vehicles with PGM-based autocatalysts competitively priced compared to the electric vehicle alternatives.

The market has become progressively more bearish on Battery Electric Vehicle (BEV) growth rates recently. Previously, annual growth in excess of 30% off a small base had been expected. While the premium sector has electrified to a greater extent, adoption lags in the mass market driven by price, which is not likely to converge with ICE prices in the near term. In addition, challenging macro factors (inflation, limited discretionary spend, high borrowing costs) are also constraining new vehicle purchases. In expansive geographies such as North America, range anxiety abounds in areas where infrastructure has lagged and installing larger batteries to counter this exacerbates the cost issue. BEVs are approximately 30% more expensive, have higher insurance costs and lower resale values than an equivalent ICE and it is expected that hybrids (with similar PGM loadings to ICE) will benefit from these factors. Starting in H2 2023, signs of softer demand for BEVs materialised despite more models coming to market and improved government incentives. This has resulted in slower production ramp-up and delayed capital investments by many OEMs as profitability and returns are under pressure. Increased restrictions on the US IRA subsidies from 2024 will negatively impact OEM margins with costs being passed on to consumers. Finally, as many key economies hold elections this year, there is significant uncertainty around environmental and economic policies that could impact the mix of "future power trains". We expect BEV growth rates to slow over the medium term, with ICE hybrids increasing over the same period.

The European Commission announced some €7 billion funding for over 30 hydrogen projects through the Important Projects of Common European Interest (IPCEI) initiative in mid-February. This included additional electrolyser deployment for renewable hydrogen production and construction of further Liquid Organic Hydrogen Carrier (LOHC) terminal capacity for handling hydrogen. Whilst PGM-based technologies are only involved in some of these projects, this is nonetheless positive for demand growth (mainly platinum, iridium, and ruthenium) in the hydrogen economy.

Battery Metals market update

Lithium

Gross lithium demand is estimated to have increased by 42% last year, primarily driven by greater demand from the battery sector. Growing BEV and PHEV production and larger battery pack sizes led to a 55% rise in lithium consumed in automotive lithium-ion batteries, accounting for over 90% of overall growth.

China was the primary driver of global automotive demand growth once again, comprising 40% of growth in 2023, despite a slower growth in BEV sales compared to the year before. China’s BEV production expanded by 29% to nearly 7 million units last year, while domestic BEV sales continued to increase robustly, albeit at a slower pace than in 2022, owing to weaker consumer confidence caused by a worsening macroeconomic outlook and price wars. Lithium consumption also grew robustly in the US and Europe and global BEV production rose by 39% to more than 11 million units.

Primary lithium supply is estimated to have increased by 51% in response to high prices prevailing in recent years, with new supply outpacing demand for the first time since 2018 and pushing the market into a primary surplus. The majority of this additional supply came from Australia, Chile and China, with Brazil, Africa and North America also beginning to emerge as notable sources of supply. As a result of growth in primary supply and destocking of accumulated inventory in China, lithium carbonate prices fell by 82% from close to $70,000/t at the start of 2023 to around $12,000/t at the end the year.

Lithium demand is forecast to increase by a more muted 29% for 2024, largely owing to continued growth in the BEV segment, especially in China. With additional growth in lithium supply expected from expansion of production in Australia, China, Africa and Argentina, prices are likely to remain subdued for 2024, albeit above historical levels, before rising over the medium term as the market balance begins to tighten once again.

While prices should continue to incentivise projects at quality assets, pauses in investment and other delays may lead to a lag in supply growth further out, and shortfalls are therefore expected to re-emerge from 2026/27 as demand growth outstrips expansion in supply.

Nickel

In 2023, global demand for nickel rose 5%, as demand for mobility batteries continued to increase rapidly. Battery demand is estimated to have increased by more than 25% last year, largely thanks to strong growth in BEV sales in China, which reached 6.68 million units. Despite the rising market share of lithium iron phosphate batteries in the Chinese market, the greater energy density of high-nickel NMC batteries is supporting demand in the European and North American markets. Stainless steel demand was stable year-on-year in 2023, rising marginally to just over 3 million tonnes.

The nickel market was in surplus in 2023 as global nickel supply increased significantly. This was mainly as a result of nickel pig iron and mixed hydroxide precipitate (MHP) production expansion in Indonesia. The sharp increase in supply has depressed benchmark nickel prices and caused the value of nickel in battery-grade nickel sulphate to trade at a discount to LME nickel price for much of the year. Indonesian output is expected to continue to increase during 2024, extending the market surplus.

The LME nickel price averaged $21,505/tonne for 2023, 18% lower than for 2022, and fell to $16,375/tonne by the end of the year. The price volatility caused by the invasion of Ukraine has subsided, and the shift in focus from a tight class 1 market to oversupply due to Indonesian supply growth contributed to the price weakness. Lower-cost nickel production in Indonesia is undercutting the rest of global supply, and has resulted in a number of nickel operations being closed in the last few months, with more production likely to close in 2024.

Zinc

The zinc price (LME Cash Settlement Price) started relatively high at US$3,289/tonne in January 2023 then dropped to US$2,502/tonne in December 2023. Chinese smelters, which comprise approximately 50% of global smelting capacity, reported record production for 2023 .

A decline in zinc prices in 2023 triggered the suspensions and closures of a number of zinc mines. This resulted in tightness in the zinc concentrate market which contributed to a fall in Treatment Charges (TC’s) for zinc concentrate below the 2023 annual benchmark of US$274/tonne. By the end of 2023, spot TC’s had fallen to below US$100/tonne.

Although inflationary pressures in several of the world’s major economies appear to be easing, global supply chains may not fully normalise due to geopolitical tensions and conflicts in 2024. Globally, zinc miners’ margins remain under pressure. However, an expected bounce back in demand mainly driven by China, India and a moderate recovery in Europe, together with delayed new mine projects and expansions due to financial and technical issues, should be positive for zinc markets in 2024. Zinc concentrate supply is expected to be tight in the first half of 2024, resulting in low spot TC’s.

These factors are expected to be supportive of stronger zinc prices across 2024 compared to current levels. In addition, market expectations are that 2024’s annual benchmark TC’s will be lower than last year’s US$274/tonne, and a better year for zinc miners should be expected.

STRATEGIC REVIEW

A disciplined focus on capital allocation was maintained during the year. Despite the significant pressure on commodity prices, with the exception of gold, market valuations have been slow to retrace until very recently, and whilst we continue to evaluate opportunities, the primary M&A focus has been on the circular economy where valuations have become more reasonable, and in line with our strategy. Our involvement in the process to extend our copper portfolio into Zambia through our bid to acquire the Mopani operation was unsuccessful. We remain interested in increasing our exposure to copper at an opportune time including through progressing feasibility studies for Mt Lyell.

In January the Rhyolite Ridge lithium/boron project in Nevada was awarded a conditional loan of US$700 million from the US Department of Energy, a strong endorsement of the project. The project is in the final stages of the federal permitting process with a record of decision expected in Q4 2024. While the focus is on getting the South basin into production, the option we have on the North basin offers a vast footprint providing scalability in future. Provided Rhyolite Ridge meets the conditions precedent, it is expected that Sibanye-Stillwater could commence funding of the staged US$490 million (R9.4bn*) JV contribution in H2 2024. With a minimum two year lead time from start of construction, the earliest that Rhyolite Ridge could commence operations would be late 2026.

The integration of New Century Resources, with majority ownership acquired on 22 February 2023 and 100% ownership on 15 May 2023, has progressed well with restructuring carried out to optimise regional and operational efficiencies. With Century zinc tailings retreatment operations operating well, the focus has moved onto exploring regional opportunities. In November the Group exercised the option to acquire 100% of the Mt Lyell Copper Project (a previously operated copper mine) located in Tasmania, Australia. The Mt Lyell feasibility study (AACE Class 3 Estimate) is expected to be finished in H1 2024.

We announced in November that we had brought forward the completion of the transaction entered into between Rustenburg Platinum Mines Limited (RPM) a subsidiary of Anglo American Platinum Limited (AAP), and Sibanye-Stillwater’s subsidiary, Sibanye Rustenburg Platinum Mines Limited (Rustenburg operation) which was originally announced on 31 January 2022, resulting in the Rustenburg operation acquiring RPM’s 50% share in the Kroondal pool and share agreement (Kroondal PSA) and the Group assuming full ownership of the low cost, mechanised Kroondal operation, effective 1 November 2023.

RPM will be paid a deferred consideration (Deferred Consideration) calculated from 1 November 2023 until the full contracted 1,350,000 4Eoz (100% basis) have been delivered, which is expected to be during Q2 2024 (the Deferred Period). Further detail on the transaction is available at: (https://thevault.exchange/?get_group_doc=245/1698843217-ssw-Kroondal-PSA-early-close-01nov2023.pdf). The remaining ounces (approx. 231,009 4E as at end September 2023) will continue to be delivered under the terms of the current Kroondal operation purchase of concentrate (PoC) agreement. Upon delivery of the final remaining ounces, the PoC will fall away and all PGM concentrate from the Kroondal operation, will be subject to the terms of the current Rustenburg operation’s sale and toll treatment agreement with RPM.

This transaction is a smart and value accretive transaction for all stakeholders. By consolidating the mining area with the adjacent Rustenburg operations under a single operator, the operating life of the Kroondal operation will be extended by extracting adjacent Rustenburg resources from the mechanised and low-cost Kroondal operation adding approximated 1.7 million 4Eoz extra production over the life-of-mine. Accelerating the extraction of more remote parts of the Rustenburg operation orebody will also unlock significant value by realising financial benefits many years earlier, sustaining employment for an extended period and enabling the creation of significant shared value for all stakeholders in the region.

During 2023, through our BioniCCube investment vehicle, we made investments in Verkor €15 million (R299 million), Glint £1.3 million (R31 million) and other (including Enhywhere) ~ €1 million (R16 million).

In line with the focus on the circular economy, we are optimistic that the acquisition of Reldan will be concluded for an estimated cash consideration of US$155.4m (R3.0 billion*) in March 2024. It is anticipated that the transaction will be value accretive and positively contribute to Sibanye-Stillwater from day one. The financing will be provided by the opportunistic and well timed US$500 million senior unsecured guaranteed convertible bond due in 2028, which we completed in November 2023, paying a low coupon of 4.25% per annum. This offering was multiple times oversubscribed and was one of various available financing options, which provided financial flexibility at a reasonable cost under market conditions, and will enable further delivery on our strategic growth objectives at an opportune time in the commodity cycle, whilst maintaining balance sheet resilience and liquidity.

While we continue to look at selective M&A which will complement our existing business, our focus for now is on the Group’s strategic essentials with a major focus on reducing both operating and capital costs and improving efficiencies whilst managing our operating entities and projects using the existing balance sheet.

* Based on the closing exchange rate of R19.25/US$ at 29 February 2024 from EquityRT

OPERATING GUIDANCE FOR 2024*

The US PGM operations forecast production of between 440,000 2Eoz and 460,000 2Eoz, with AISC of between US$1,365/2Eoz to US$1,425/2Eoz excluding any possible S45X credit (45X Advanced Manufacturing Production Credit (S45X credit), with a capital reduction. Capital expenditure is forecast to be between US$175 million and US$190 million, including approximately US$13 million project capital.

3E PGM production for the US PGM recycling operations is forecast to be between 300,000 and 350,000 3Eoz fed for 2024. Capital expenditure is forecast at US$700,000 (R12 million).

4E PGM production from the SA PGM operations for 2024 is forecast to be between 1.8 million 4Eoz and 1.9 million 4Eoz including approximately 80,000 4Eoz of third party PoC, with AISC between R21,800/4Eoz and R22,500/4Eoz (US$1,245/4Eoz and US$1,285/4Eoz) – excluding cost of third party PoC. Capital expenditure is forecast at R6.0 billion (US$343 million)* for the year.

Gold production from the managed SA gold operations (excluding DRDGOLD) for 2024 is forecast at between 19,500kg (627koz) and 20,500kg (659koz). AISC is forecast to be between R1,100,000/kg and R1,200,000/kg (US$1,955/oz and US$2,133/oz). Capital expenditure is forecast at R3.9 billion (US$223 million), including R390 million (US$22 million) of project capital expenditure provided for the Burnstone project.

Production from the Sandouville nickel refinery is forecast at between 7.5 and 8.5 kilotonnes of nickel product, at a Nickel equivalent sustaining cost of between €21,000/tNi (R399k/tNi)* and €23,000/tNi (R437k/tNi)* and capital expenditure of €8 million (R152 million)*. Capital expenditure at the Keliber lithium project for 2023 is forecast to be about €361 million (R6.9 billion)*.

Production from the Century zinc tailings retreatment operation is forecast at between 87 and 100 kilotonnes of zinc metal (payable) at an AISC of between A$3,032 and A$3,434/tZn (US$/2,032 and US$2,302/tZn/ R35,560 and R40,285/tZn) and capital expenditure of A$17 million (US$11 million or R196 million). Project capital on the Mount Lyell copper/gold project for 2024 is forecast to be A$6.6 million (US$4 million or R77 million).

*The guidance has been translated where relevant at an average exchange rate of R17.50/US$, R19.00/€ and R11.73/A$

NEAL FRONEMAN

CHIEF EXECUTIVE OFFICER

This is a short form of the news created by SRC swiss resource capital AG! Only the full English original version is valid!

ADMINISTRATION AND CORPORATE INFORMATION

SIBANYE STILLWATER LIMITED

(SIBANYE-STILLWATER)

Incorporated in the Republic of South Africa

Registration number 2014/243852/06

Share code: SSW and SBSW

Issuer code: SSW

ISIN: ZAE000259701

LISTINGS

JSE: SSW

NYSE: SBSW

WEBSITE

www.sibanyestillwater.com

REGISTERED AND CORPORATE OFFICE

Constantia Office Park

Bridgeview House, Building 11, Ground floor,

Cnr 14th Avenue & Hendrik Potgieter Road

Weltevreden Park 1709

South Africa

Private Bag X5

Westonaria 1780

South Africa

Tel: +27 11 278 9600

Fax: +27 11 278 9863

COMPANY SECRETARY

Lerato Matlosa

Email: lerato.matlosa@sibanyestillwater.com

DIRECTORS

Dr Vincent Maphai* (Chairman)

Neal Froneman (CEO)

Charl Keyter (CFO)

Dr Elaine Dorward-King*

Harry Kenyon-Slaney*^

Jeremiah Vilakazi*

Keith Rayner*

Nkosemntu Nika*

Richard Menell*

Savannah Danson*

Susan van der Merwe*

Timothy Cumming*

Sindiswa Zilwa*

* Independent non-executive

^ Lead independent director, appointed January 2024

INVESTOR ENQUIRIES

James Wellsted

Executive Vice President: Investor Relations and Corporate Affairs

Mobile: +27 83 453 4014

Email: james.wellsted@sibanyestillwater.com

or ir@sibanyestillwater.com

In Europe:

SRC swiss resource capital AG

Jochen Staiger & Marc Ollinger

info@resource-capital.ch

JSE SPONSOR

JP Morgan Equities South Africa Proprietary Limited

Registration number 1995/011815/07

1 Fricker Road

Illovo

Johannesburg 2196

South Africa

Private Bag X9936

Sandton 2146

South Africa

AUDITORS

Ernst & Young Inc. (EY)

102 Rivonia Road

Sandton 2196

South Africa

Private Bag X14

Sandton 2146

South Africa

Tel: +27 11 772 3000

AMERICAN DEPOSITARY RECEIPTS

TRANSFER AGENT

BNY Mellon Shareowner Correspondence (ADR)

Mailing address of agent:

Computershare

PO Box 43078

Providence, RI 02940-3078

Overnight/certified/registered delivery:

Computershare

150 Royall Street, Suite 101

Canton, MA 02021

US toll free: + 1 888 269 2377

Tel: +1 201 680 6825

Email: shrrelations@cpushareownerservices.com

Tatyana Vesselovskaya

Relationship Manager – BNY Mellon

Depositary Receipts

Email: tatyana.vesselovskaya@bnymellon.com

TRANSFER SECRETARIES SOUTH AFRICA

Computershare Investor Services Proprietary Limited

Rosebank Towers15 Biermann Avenue

Rosebank 2196

PO Box 61051

Marshalltown 2107South Africa

Tel: +27 11 370 5000

Fax: +27 11 688 5248

DISCLAIMER

FORWARD LOOKING STATEMENTS

The information in this document may contain forward-looking statements within the meaning of the “safe harbour” provisions of the United States Private Securities Litigation Reform Act of 1995 with respect to Sibanye Stillwater Limited’s (Sibanye-Stillwater or the Group) financial condition, results of operations, business strategies, operating efficiencies, competitive position, growth opportunities for existing services, plans and objectives of management for future operations, markets for stock and other matters. These forward-looking statements, including, among others, those relating to Sibanye-Stillwater’s future business prospects, revenues and income, expected cost savings and capital reduction/deferral, climate change-related targets and metrics, the potential benefits of past and future acquisitions (including statements regarding growth, cost savings, benefits from and access to international financing and financial re-ratings), gold, PGM, nickel and lithium pricing expectations, levels of output, supply and demand, information relating to Sibanye-Stillwater’s new or ongoing development projects, any proposed, anticipated or planned expansions into the battery metals or adjacent sectors and estimations or expectations of enterprise value, adjusted EBITDA and net asset, are necessarily estimates reflecting the best judgment of the senior management and directors of Sibanye-Stillwater and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements. As a consequence, these forward-looking statements should be considered in light of various important factors, including those set forth in this document.

All statements other than statements of historical facts included in this document may be forward-looking statements. Forward-looking statements also often use words such as “will”, “would”, “expect”, “forecast”, “goal”, “vision”, “potential”, “may”, “could”, “believe”, “aim”, “anticipate”, “target”, “estimate” and words of similar meaning. By their nature, forward-looking statements involve risk and uncertainty because they relate to future events and circumstances and should be considered in light of various important factors, including those set forth in this disclaimer. Readers are cautioned not to place undue reliance on such statements.

The important factors that could cause Sibanye-Stillwater’s actual results, performance or achievements to differ materially from estimates or projections contained in the forward-looking statements include, without limitation, Sibanye-Stillwater’s future financial position, plans, strategies, objectives, capital expenditures, projected costs and anticipated cost savings, financing plans, debt position and ability to reduce debt leverage; economic, business, political and social conditions in South Africa, Zimbabwe, the United States, Europe, Australia and elsewhere; plans and objectives of management for future operations; Sibanye-Stillwater’s ability to obtain the benefits of any streaming arrangements or pipeline financing; the ability of Sibanye-Stillwater to comply with loan and other covenants and restrictions and difficulties in obtaining additional financing or refinancing; Sibanye-Stillwater’s ability to service its bond instruments; changes in assumptions underlying Sibanye-Stillwater’s estimation of its Mineral Resources and Mineral Reserves; any failure of a tailings storage facility; the ability to achieve anticipated efficiencies and other cost savings in connection with, and the ability to successfully integrate, past, ongoing and future acquisitions, as well as at existing operations; the ability of Sibanye-Stillwater to complete any ongoing or future acquisitions; the success of Sibanye-Stillwater’s business strategy and exploration and development activities, including any proposed, anticipated or planned expansions into the battery metals or adjacent sectors and estimations or expectations of enterprise value (including the Rhyolite Ridge project); the ability of Sibanye-Stillwater to comply with requirements that it operate in ways that provide progressive benefits to affected communities; changes in the market price of gold, PGMs, battery metals (e.g., nickel, lithium, copper and zinc) and the cost of power, petroleum fuels, and oil, among other commodities and supply requirements; the occurrence of hazards associated with underground and surface mining; any further downgrade of South Africa’s credit rating; the impact of South Africa’s greylisting; a challenge regarding the title to any of Sibanye-Stillwater’s properties by claimants to land under restitution and other legislation; Sibanye-Stillwater’s ability to implement its strategy and any changes thereto; the outcome of legal challenges to the Group’s mining or other land use rights; the occurrence of labour disputes, disruptions and industrial actions; the availability, terms and deployment of capital or credit; changes in the imposition of industry standards, regulatory costs and relevant government regulations, particularly environmental, sustainability, tax, health and safety regulations and new legislation affecting water, mining, mineral rights and business ownership, including any interpretation thereof which may be subject to dispute; increasing regulation of environmental and sustainability matters such as greenhouse gas emissions and climate change; being subject to, and the outcome and consequence of, any potential or pending litigation or regulatory proceedings, including in relation to any environmental, health or safety issues; the ability of Sibanye-Stillwater to meet its decarbonisation targets, including by diversifying its energy mix with renewable energy projects; failure to meet ethical standards, including actual or alleged instances of fraud, bribery or corruption; the effect of climate change or other extreme weather events on Sibanye-Stillwater’s business; the concentration of all final refining activity and a large portion of Sibanye-Stillwater’s PGM sales from mine production in the United States with one entity; the identification of a material weakness in disclosure and internal controls over financial reporting; the effect of US tax reform legislation on Sibanye-Stillwater and its subsidiaries; the effect of South African Exchange Control Regulations on Sibanye-Stillwater’s financial flexibility; operating in new geographies and regulatory environments where Sibanye-Stillwater has no previous experience; power disruptions, constraints and cost increases; supply chain disruptions and shortages and increases in the price of production inputs; the regional concentration of Sibanye-Stillwater’s operations; fluctuations in exchange rates, currency devaluations, inflation and other macro-economic monetary policies; the occurrence of temporary stoppages or precautionary suspension of operations at its mines for safety or environmental incidents (including natural disasters) and unplanned maintenance; Sibanye-Stillwater’s ability to hire and retain senior management and employees with sufficient technical and/or production skills across its global operations necessary to meet its labour recruitment and retention goals, as well as its ability to achieve sufficient representation of historically disadvantaged South Africans in its management positions; failure of Sibanye-Stillwater’s information technology, communications and systems; the adequacy of Sibanye-Stillwater’s insurance coverage; social unrest, sickness or natural or man-made disaster at informal settlements in the vicinity of some of Sibanye-Stillwater’s South African-based operations; and the impact of HIV, tuberculosis and the spread of other contagious diseases, including global pandemics.

Further details of potential risks and uncertainties affecting Sibanye-Stillwater are described in Sibanye-Stillwater’s filings with the Johannesburg Stock Exchange and the United States Securities and Exchange Commission, including the 2022 Integrated Report and the Annual Financial Report for the fiscal year ended 31 December 2022 on Form 20-F filed with the United States Securities and Exchange Commission on 24 April 2023 (SEC File no. 333-234096).

These forward-looking statements speak only as of the date of the content. Sibanye-Stillwater expressly disclaims any obligation or undertaking to update or revise any forward-looking statement (except to the extent legally required). These forward-looking statements have not been reviewed or reported on by the Group’s external auditors.

Non-IFRS Measures

The information contained in this document may contain certain non-IFRS measures, including, among others, adjusted EBITDA, adjusted EBITDA margin, AISC, AIC, Nickel equivalent sustaining cost and adjusted free cash flow. These measures may not be comparable to similarly-titled measures used by other companies and are not measures of Sibanye-Stillwater’s financial performance under IFRS. These measures should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Sibanye-Stillwater is not providing a reconciliation of the forecast non-IFRS financial information presented in this document because it is unable to provide this reconciliation without unreasonable effort. These forecast non-IFRS financial information presented have not been reviewed or reported on by the Group’s external auditors.

Websites

References in this document to information on websites (and/or social media sites) are included as an aid to their location and such information is not incorporated in, and does not form part of, this document.

Swiss Resource Capital AG

Poststrasse 1

CH9100 Herisau

Telefon: +41 (71) 354-8501

Telefax: +41 (71) 560-4271

http://www.resource-capital.ch

CEO

Telefon: +41 (71) 3548501

E-Mail: js@resource-capital.ch

![]()